United Kingdom move to regulate stablecoins and create “global hub” for cryptocurrency

[ad_1]

Another country has entered the cryptocurrency party, and it’s a big one. The United Kingdom’s Economic and Finance Ministry announced this afternoon that the country will be amending its regulatory framework to allow the introduction of stablecoins as a means of payment.

Sure, it’s not like Boris Johnson has gone full-El Salvador and introduced Bitcoin as legal tender, but it’s still an important step and one that may cause a domino effect, especially given it is coming from Britain.

The most criticised aspect of El Salvador’s Bitcoin initiative, of course, is the notorious volatility that Bitcoin suffers from. With stablecoins, that is not an issue, with their value pegged to fiat counterparts.

This is part of the reason that this announcement is such notable news – this is very much a targeted initiative looking at introducing crypto specifically as a means of payment, rather than simply loosening the overall regulation on the industry.

Her Majesty’s Treasury (otherwise referred to as the Exchequer – I’m still learning my British acronyms as I intend to move to London later this year), were quite bullish in their assessment of stablecoins in their statement Monday: “The rationale for doing this is that certain stablecoins have the capacity to potentially become a widespread means of payment including by retail customers, driving consumer choice and efficiencies”.

Her Majesty’s Treasury (otherwise referred to as the Exchequer – I’m still learning my British acronyms as I intend to move to London later this year), were quite bullish in their assessment of stablecoins in their statement Monday: “The rationale for doing this is that certain stablecoins have the capacity to potentially become a widespread means of payment including by retail customers, driving consumer choice and efficiencies”.

The statement continued that the amendment of regulation to facilitate these stablecoins was just one aspect of a “package of measures” aimed at incorporating blockchain technology into the UK and creating a “global hub” – so while payment is the first item on the list, as we just mentioned, the UK are also signalling their intent to eventually go beyond this niche and embrace the wider crypto industry, too.

With the volatility of “normal” cryptocurrencies rendering them impractical right now for commerce, stablecoins are primed to take the step up…if regulators get on board. This move by the UK, therefore, is a massive signal of intent – because it is so achievable. “If crypto technologies are going to be a big part of the future, then we – the UK – want to be in, and in on the ground floor” the Economic Secretary, John Glen, said at the Innovate Finance Global Summit. “In fact, if we commit now…if we act now…we can lead the way”, he continued.

We got thoughts from Katie Evans, DeFi Expert at Swarm Markets, on what this may mean, as an insider in the industry. “London is a massive global financial hub, and it has to keep up with the constantly-changing face of financial technology”, she said. “The UK Government does seem to be paying attention to the fact that the race is on to build the crypto centres of the next 50 years, and this is in essence its way of setting out its stall”. Evans was also enthused that stablecoins in particular were a point of focus, pointing out that they serve as “a useful on-ramp for potential crypto asset users” and are “one of the simplest to assess and approve in crypto terms, bringing them in line with existing financial markets regulation”.

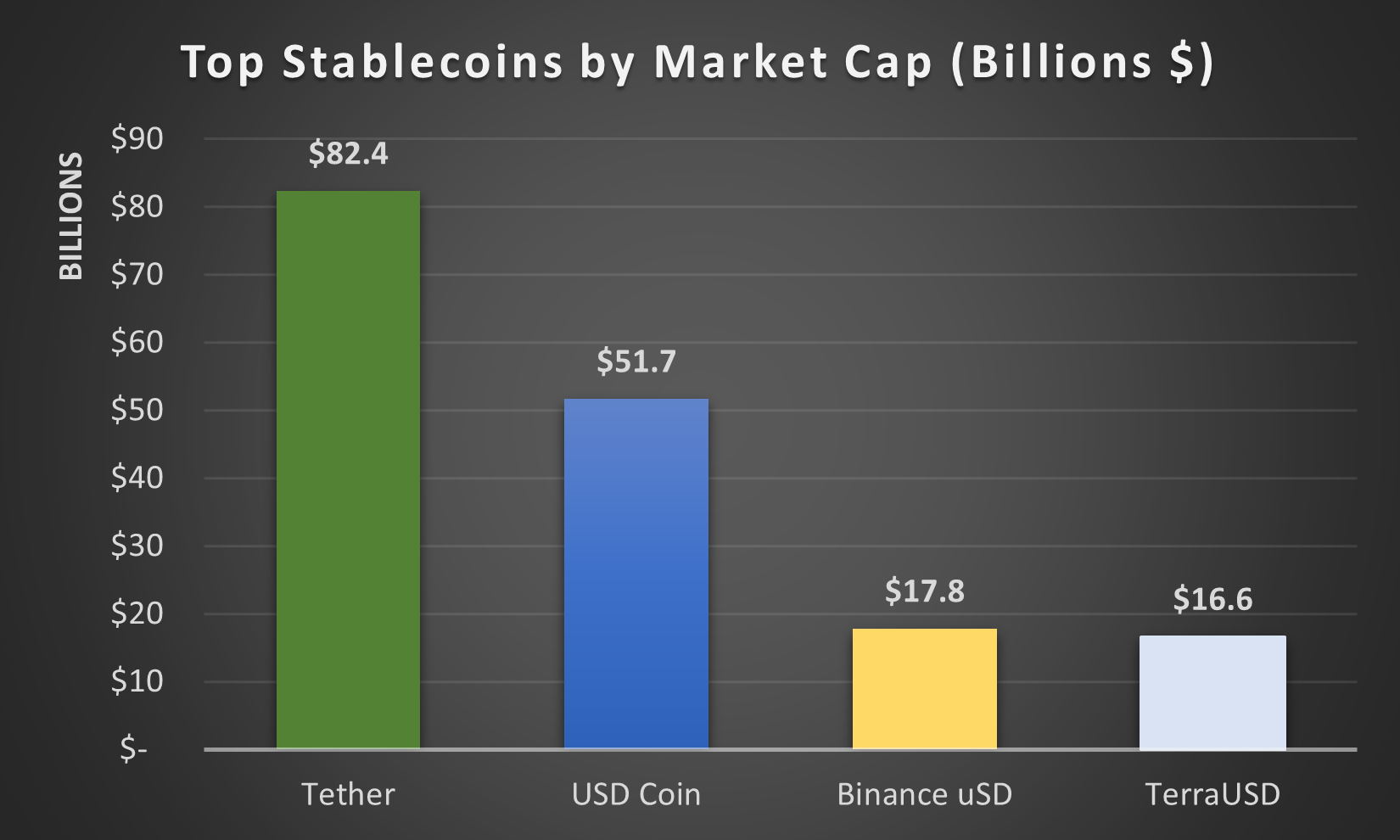

Another interesting tidbit? The non-appearance of Central Bank Digital Currencies (CBDCs) in the announcement. This is very much looking at stablecoins such as Tether, Circle etc to be used as a medium of exchange, when many would have anticipated a CBDC announcement as more likely.

It’s a big marker to lay down, as the UK are now set to become one of the first countries to provide clear guidance to the crypto industry as to how stablecoins can be implemented. This story will grow and is far from over, but today is an important first step.

[ad_2]

Source link